DSCR Calculator — Does This Rental Property Cash Flow?

Before you make an offer on a rental property, you need to know one number above everything else — your Debt Service Coverage Ratio. DSCR tells you whether the property's income covers its debt payments, and it is the primary metric lenders use to approve investment property loans.

Our free DSCR Calculator gives you an instant answer — does this property cash flow? Can you qualify for a DSCR loan on it? And what would your monthly cash flow look like after all expenses?

🏠 DSCR Calculator — Does This Rental Property Cash Flow?

Enter the property income and debt details to get your DSCR and monthly cash flow instantly

DSCR requirements vary by lender. Most require a minimum DSCR of 1.0-1.25. This calculator is an estimate — actual loan approval depends on full underwriting review.

Ready to get financing on this property? We offer DSCR loans with competitive wholesale rates and zero junk fees. No income verification required — the property qualifies itself.

Get a DSCR Loan Quote — FreeWhat Is DSCR and Why Does It Matter?

DSCR stands for Debt Service Coverage Ratio. It is calculated by dividing a property's gross rental income by its total debt service — the principal and interest payment on the mortgage.

The DSCR Formula

DSCR = Monthly Gross Rent ÷ Monthly Principal & Interest Payment

| DSCR | What It Means | Lender View |

|---|---|---|

| 1.25 or higher | Strong cash flow — rent covers debt with 25% cushion | Excellent — best rates available |

| 1.0 to 1.24 | Rent covers debt — breaking even or slightly positive | Acceptable — qualifies with most lenders |

| 0.75 to 0.99 | Rent does not fully cover debt — negative cash flow | Some lenders allow with larger down payment |

| Below 0.75 | Significant negative cash flow | Most lenders will not approve |

What Is a DSCR Loan?

A DSCR loan — also called a Debt Service Coverage Ratio loan or investor cash flow loan — is a mortgage designed specifically for real estate investors. Unlike conventional loans, DSCR loans do not require you to verify your personal income with W-2s, tax returns, or pay stubs. The property qualifies itself based on its rental income.

📋 No Income Verification

No W-2s. No tax returns. No pay stubs. The property's rental income is the qualification metric — not your personal income. This makes DSCR loans ideal for self-employed investors, those with complex tax situations, or investors with multiple properties.

🏠 Scale Your Portfolio

Conventional loans cap borrowers at 10 financed properties. DSCR loans have no such limit. Serious investors use DSCR loans to build portfolios of 20, 30, or more properties that would be impossible to finance conventionally.

⚡ Faster Closing

Without the income documentation requirements of conventional loans, DSCR loans typically close faster. Less paperwork, less back and forth — which matters when you are competing for a desirable investment property.

🌟 Short-Term Rentals

Many DSCR lenders will use Airbnb or VRBO income — based on documented rental history or a market analysis — to qualify the property. This opens up short-term rental financing that is unavailable with conventional loans.

Ken Turkington Has Investment Properties in Tempe — He Knows This Market

Our co-founder Ken Turkington owns investment properties in Tempe, Arizona and has been investing in the Phoenix metro real estate market for years. When you work with First Commerce Financial on an investment property loan, you are not talking to someone who read about it in a textbook. Ken has run these numbers on his own deals and knows exactly what makes a rental property work financially in the markets we serve.

DSCR Loans vs. Conventional Investment Property Loans

| Feature | DSCR Loan | Conventional Investment Loan |

|---|---|---|

| Income verification | Property income only | Personal W-2s and tax returns required |

| Maximum properties | Unlimited | 10 financed properties max |

| Self-employed friendly | Yes — no personal income needed | Complex — 2 years returns required |

| Minimum down payment | 20-25% | 15-25% |

| Interest rates | Slightly higher | Slightly lower |

| Short-term rental income | Often accepted | Rarely accepted |

| Closing speed | Faster | Slower |

Investment Property Markets We Serve

We originate DSCR and investment property loans across all four of our licensed states — each with strong rental market fundamentals:

Arizona — Phoenix Metro

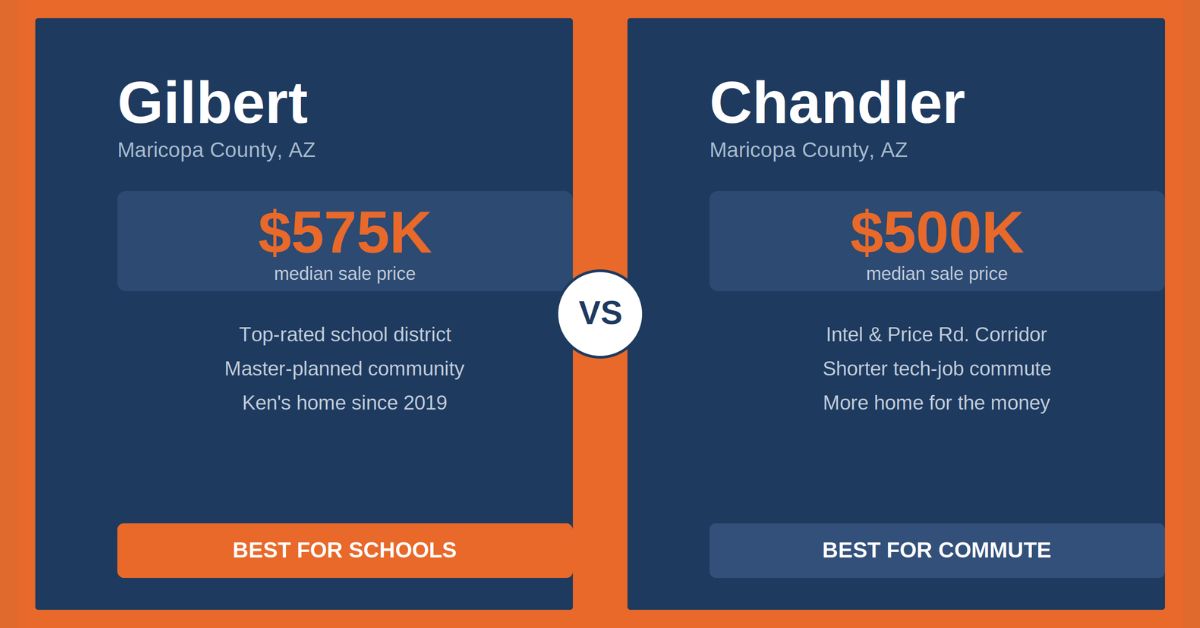

Gilbert, Tempe, Chandler, Queen Creek, Mesa, and Scottsdale are all strong rental markets with population growth, job growth, and consistent rental demand. Ken owns investment properties in Tempe and actively invests in the Phoenix metro. Apache Junction was the #1 ZIP code in the Phoenix metro on the 2025 Zonda Heat Index.

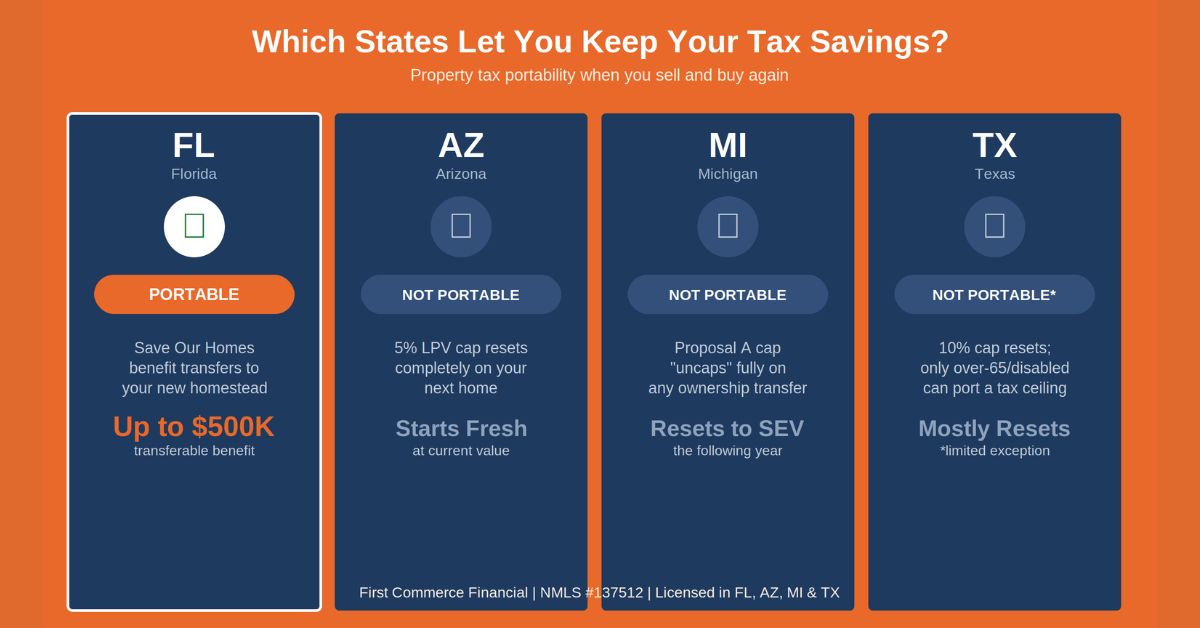

Florida — Jacksonville and Lakewood Ranch

Northeast Florida and the Sarasota-Bradenton corridor are among the strongest rental markets in the Southeast. NAS Jacksonville and Naval Station Mayport drive consistent demand from military families. Lakewood Ranch continues to attract relocating buyers which supports strong rental demand for transitional housing.

Michigan — Metro Detroit

Metro Detroit offers some of the most attractive cap rates of any major market in the country. Lower acquisition costs relative to rent mean DSCR ratios are often stronger here than in coastal markets. Novi, Commerce Township, Brighton, and the broader Oakland and Washtenaw County markets have strong long-term rental demand.

Texas

Texas has no state income tax, strong population growth, and some of the most landlord-friendly laws in the country. We originate investment property loans throughout our Texas markets.

More Tools for Real Estate Investors

🏠Full Investment Property Calculator Suite — DSCR, Fix and Flip, and More 💰Net Proceeds Calculator — How Much Will You Make When You Sell? 📈Closing Cost Estimator — See Every Fee Before You Close 🔧All Free Tools and CalculatorsWhat credit score do I need for a DSCR loan?

Most DSCR lenders require a minimum 620-640 credit score. Better credit scores unlock lower rates. A 700+ credit score will give you access to the best DSCR loan pricing available. Unlike conventional loans where credit score is one of many factors, DSCR loans put more weight on credit score since there is no income verification — your score becomes even more important.

Can I use projected rent instead of actual rent to qualify?

Yes — many DSCR lenders will use a market rent analysis from an appraiser rather than requiring an existing lease. This is useful for properties that are currently vacant, owner-occupied, or being purchased as a new rental. The appraiser will provide a rent schedule showing the market rent for the property which the lender uses for DSCR calculation.

Can I use a DSCR loan for a short-term rental like Airbnb?

Many DSCR lenders accept short-term rental income — using either documented STR history from platforms like Airbnb or VRBO, or a market analysis of comparable short-term rental income. Rules vary by lender and market. Some markets have restrictions on short-term rentals that affect financing — we will review the specific property and market and find the right lender for your situation.

How is a DSCR loan different from a hard money loan?

DSCR loans are long-term permanent financing — 30-year fixed rates comparable to conventional investment loans, just without the income verification. Hard money loans are short-term bridge financing — typically 12-24 months, higher rates, used for acquisition and renovation before refinancing into permanent financing. If you are buying a stabilized rental property you plan to hold, a DSCR loan is almost always the right tool. If you are buying a distressed property to renovate, a hard money or fix and flip loan is the starting point.

Ready to Finance Your Next Investment Property?

We offer DSCR loans with competitive wholesale rates and zero junk fees across Michigan, Florida, Arizona, and Texas. No income verification, no W-2s, no tax returns — the property qualifies itself. Talk to Kirk or Ken directly and get a quote same day.

Get a Free DSCR Loan QuoteRelated Posts